How Does Credit Score Work?

Every business needs funds at some point. You may want to buy more stock, expand operations, manage cash flow or grab a new opportunity. Whatever the reason, your credit score plays an important role when you apply for a loan.

But what is a credit score? How credit score works? Why do lenders check it before offering a business loan? And how can you know your credit score in a simple way.

At TallyCapital, we simplify complex credit concepts so business owners can clearly understand what lenders look for and how to improve their chances of loan approval.

What is a Credit Score

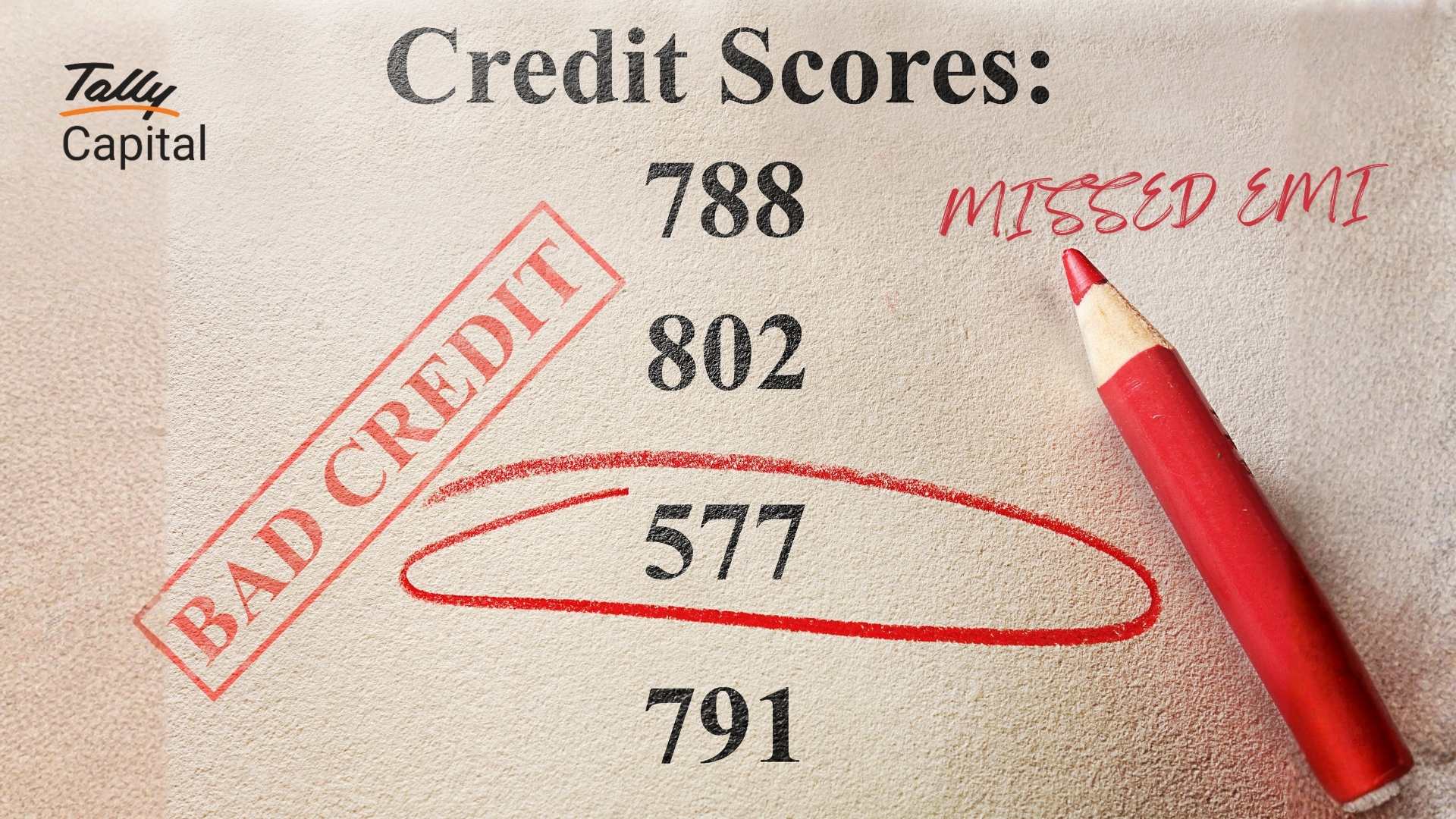

A credit score is a three-digit number that indicates how trustworthy you are as a borrower. It tells the lender how likely you are to repay a loan on time. Think of it as your financial report card.

In India, the score usually ranges from 300 to 900.

- A higher score shows strong credit behaviour

- A lower score shows a higher risk

If you want easy loan approval, a smooth borrowing experience, and better interest rates, keeping a good credit score helps.

Who Calculates Your Credit Score

Your credit score is created by licensed credit bureaus. Banks and lenders share your credit information with these bureaus, and they calculate your score based on your repayment behaviour.

The four major credit bureaus in India are:

- CRIF High Mark

- TransUnion CIBIL

- Experian

- Equifax

Each bureau has its own method of calculation but they all look at similar data such as how you repay loans, how much credit you use and how frequently you apply for new credit. Lenders pull your score from one or more of these bureaus whenever you apply for a loan.

How Does Credit Score Work

Credit scoring is essentially a statistical, risk-evaluation exercise. Lenders or credit bureaus assess a borrower’s credit history using several key factors and each factor reflects a different aspect of borrowing behaviour. Then, using a proprietary algorithm or model, they combine the factors to produce a three-digit score (in India usually between 300 and 900).

Here’s a breakdown of these factors and how they influence your credit score:

Repayment history

This is the most important factor. If you pay all your EMIs and credit card bills on time, your score stays healthy. If you delay or miss payments, your score drops.

Credit usage

This shows how much of your available credit you use. For example, if you have a credit card limit of ₹1,00,000 and you use around ₹80,000 every month, your utilization is 80 percent which is considered high. Experts suggest using less than 30 percent of your credit limit.

Length of credit

If you have been using credit for many years and have a stable record, it increases your score. A long and clean history shows reliability.

Type of credit

A healthy mix of secured loans such as business loans or auto loans and unsecured credit such as credit cards shows responsible borrowing behavior.

Number of loan enquiries

Every time you apply for a loan, lenders check your credit report. Too many such checks in a short time may show that you are credit hungry which can reduce your score.

Factors That Influence the Score at a Glance

Here is a quick table to make it easier to understand.

| Factor | What It Means | Impact on Score |

|---|---|---|

| Repayment behaviour | Timely payment of EMIs and credit cards | Very high |

| Credit usage | Portion of credit limit used | High |

| Length of credit | How long you have handled credit | Medium |

| Credit mix | Variety of loans (secured & unsecured) | Medium |

| Loan enquiries | Applications for new loans or credit cards | Medium |

Why Credit Score Matters for Business Loans

When you apply for a business loan, lenders want to understand one thing.

Are you a safe borrower?

Your credit score helps them decide that. Here is why it is important.

- Banks approve loans faster when your score is good

- You get better interest rates

- You can qualify for a larger loan amount

- Lenders trust you more

- Your application process becomes smoother

Even if your business has good revenue, a low score may create hurdles in loan approval.

How to Know Credit Score Easily

There are many ways to check your score but the simplest option for business owners is through TallyCapital.

You can check your credit score directly inside the TallyPrime platform and get clear insights about your credit health.

You can also check your score on the TallyCapital website by entering basic details like name, mobile number, email and PAN. This helps you understand where you stand before applying for a loan.

Other ways include checking through credit bureau websites, but TallyCapital makes the entire experience faster and easier.

What Can Reduce Your Credit Score

Even small mistakes can affect your score. Some common reasons are:

- Missing EMIs

- Delayed bill payments

- Paying only the minimum amount on credit cards

- Using almost your full credit limit every month

- Applying for too many loans

- Closing old accounts suddenly

- Defaulting or settling old loans

Understanding these habits can help you avoid score drops in the future.

How to Improve Your Credit Score

Improving a credit score is not difficult. It requires steady behaviour and regular checkups.

Here are simple steps you can start today.

- Pay all EMIs and credit card bills before the due date

- Keep your credit usage within thirty percent

- Avoid applying for many loans at the same time

- Check your credit report regularly for errors

- Do not close old credit accounts unless necessary

- Maintain a mix of secured and unsecured loans

- Use auto payment reminders to avoid missed EMIs

Most scores begin to improve within three to six months if you follow these habits.

Personal Score and Business Score

Many small business owners use the same financial identity for both personal and business purposes. Because of this, lenders often check both your personal credit score and your business credit score.

A business credit score is affected by:

- Age of the business

- Business registration details

- Revenue patterns

- Existing business loans

- Payments to suppliers and vendors

- Consistency of transactions

- Owner or partner credit history

Both scores matter for loan approval especially for MSME and small businesses.

TallyCapital Makes the Loan Journey Simpler

TallyCapital is built for TallyPrime users who want fast and trusted business financing. It brings simple, smart and superior lending inside your Tally software so you can access funds without jumping between multiple platforms.

Here is how it works in four easy steps.

Check eligibility

You get instant insights about your loan eligibility and credit strength.

Apply with a few clicks

A simple and smooth application process within your trusted TallyPrime with minimal paperwork.

Quick approval

Fast decisions from multiple trusted lending partners.

Funds transferred directly

The loan amount is sent straight to your business account.

TallyCapital does not look only at your credit score. It also considers your business data in TallyPrime, which helps lenders take a fair and complete decision. This makes it possible for even a business with a moderate score to receive suitable loan options.

Why Businesses Prefer TallyCapital

- Smart credit score insights

- Multiple lending partners for better offers

- Access from your trusted TallyPrime platform

- Safe and transparent loan process

- Faster approvals with minimal effort

This helps businesses grow without stress or delays.

Final Thoughts

Your credit score is an important part of your financial journey. It affects how easily you can get loans and how much you pay in interest. Understanding how credit score works and how to know your credit score gives you the power to make better financial decisions.

With TallyCapital, you can check your score, get insights and access loan offers all from one trusted place. This makes financing simpler, smarter and more supportive for your business.

FAQs on How Credit Score Work

Q1. How is credit score calculated for business owners?

A credit score is calculated using repayment history, credit usage, credit mix, length of credit history and loan enquiries.

Q2. What is a good credit score for getting a business loan?

A score of 700+ is ideal for fast approvals and better interest rates, but lenders may offer loans even with moderate scores depending on your business data.

Q3. Does checking my own credit score reduce it?

No. Checking your score through TallyCapital is a soft enquiry and does not impact your score.

Q4. How long does it take to improve a credit score?

Most business owners see improvement within 3–6 months with consistent repayment and controlled credit usage.

Q5. Can I get a business loan with a low credit score?

Yes, depending on lender policies. TallyCapital also evaluates business data in TallyPrime, giving a more complete picture.

Latest Blogs

Missed EMI Impact on Credit Score:Every Borrower Must Know

How Personal Credit Score Affects Business Loan Approval

Credit Score for Business Loans: Get Faster Disbursals

What Causes a Sudden Drop in Credit Score? Common Reasons Explained

Credit Score Guide for Small Business Owners in India

9 Credit Score Mistakes MSME Owners Make